Introduction

Singapore has, in the past decade, emerged as a jurisdiction of choice for high-net-worth families to set up family offices for succession planning and the professional management of their private wealth. This trend has undoubtedly been the product of Singapore’s position as a global financial hub, its strategic location and connectivity, its political stability and clear laws and regulations on tax and trusts. Riding on the wave of rapid wealth creation in Asia, Singapore has seen the number of family offices based here grow five-fold from 2017 to 2019, with the result that there currently exists in excess of 400 single family offices in Singapore.

In a bid to enhance the attractiveness of Singapore as a jurisdiction for high-net-worth families to set up their family offices, the government of Singapore had made available two tax incentive schemes (the Section 13R and 13X schemes) under the Income Tax Act where exemption of income would apply to the following:

- Income of a company incorporated and resident in Singapore that arises from funds managed by a fund manager in Singapore (the Section 13R scheme); and

- Income arising from funds managed by a fund manager in Singapore (the Section 13X scheme).

By the issuance of a new set of guidelines titled “S13O & S13U Application Process for Family Offices – Guidelines for Advisors” (the “New Guidelines”) on 11 April 2022, the Monetary Authority of Singapore (“MAS”) has updated the conditions and procedural requirements for the aforementioned tax incentive schemes. Most significantly, the New Guidelines have laid down more stringent criteria for family offices seeking to avail themselves of the tax incentives available under what was previously referred to as the Section 13R and 13X schemes (and which are currently referred to as the Section 13O and 13U schemes).

Applicability of New Guidelines and Criteria

The New Guidelines will only apply to funds which are managed or advised directly by a family office which:

- Is an exempt fund management company which manages assets for or on behalf of the family or families; and

- Is wholly owned or controlled by members of the same family or families.

The term “family” used in this context has been defined by MAS as referring to individuals who are lineal descendants from a single ancestor, as well as the spouses, ex-spouses, adopted children and step-children of these individuals. For clarity, these New Guidelines do not apply to fund vehicles which hold assets for or on behalf of third parties outside of the family(ies) which own or control the fund vehicles. This would include fund vehicles managed by licensed fund managers such as multi-family offices and institutional fund managers and funds managed by other licence exempt managers for immovable assets.

Summary of Updated Conditions for the Section 13O & 13U Schemes

Comparison of Updated Conditions to Previous Conditions Under S13R & S13X Schemes

A. Minimum Assets Under Management

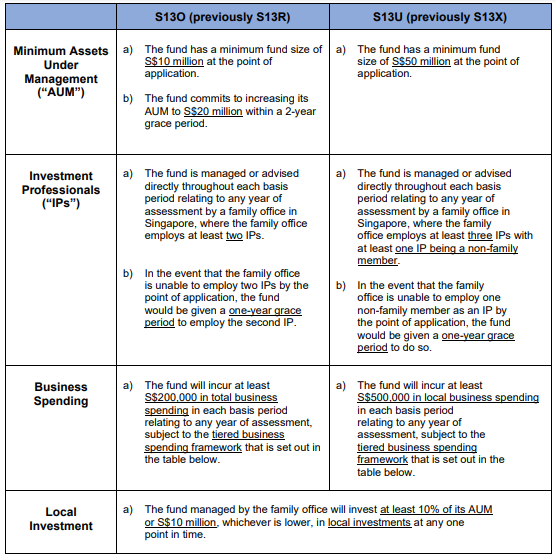

The most obvious and perhaps significant change to the conditions for the Section 13O Tax Incentive Scheme (“S13O Scheme”) relates to the minimum assets under management to qualify for the tax incentives. Where the S13O Scheme did not previously specify a minimum sum for assets under management, the updated conditions currently provide that:

- The fund has a minimum fund size of S$10 million at the point of application; and,

- That the fund commits to increasing its AUM to S$20 million within a 2-year grace period.

While the updated conditions provide greater clarity on the threshold amount to be met in assets under management to qualify for the S13O Scheme, they also raise the bar on the amount of assets under management previously regarded as necessary to qualify for the S13O Scheme.

B. Investment Professionals

The updated conditions specify the minimum number of investment professionals that an applicant must have advising and managing it to qualify for incentives under the S13O and S13U Schemes. The updated conditions also provide clarity on the qualifications that the investment professionals engaged by the family offices managing the funds must possess.

Under the S13O Scheme, the fund must now be managed or advised directly throughout each year of assessment by a family office in Singapore, where the family office employs at least two Investment Professionals. In this regard, the Investment Professionals are required to be either portfolio managers, research analysts or traders who:

- Are earning more than S$3,500 per month; and,

- must be engaging substantially in the qualifying activity.

If the family office is unable to employ two Investment Professionals at the point of application for the S13O Scheme, the fund can be given a one-year grace period to employ the second Investment Professional.

Under the S13U Scheme, the fund must also be managed or advised directly throughout the year by a family office in Singapore, albeit by a family office which employs at least three Investment Professionals (with identical qualification requirements as those specified under the S13O Scheme) wherein at least one of the three Investment Professionals must be a non-family member of the beneficial owner(s).

If the family office is unable to employ a non-family member as an Investment Professional at the point of application for the S13U Scheme, the fund can be given a one-year grace period to fill this role.

C. Business Spending

Prior to the updated conditions coming into effect, funds under the S13O Scheme were required to incur at least S$200,000 in business spending in each financial year while funds under the S13U Scheme were required to incur at least S$200,000 in local business spending in each financial year.

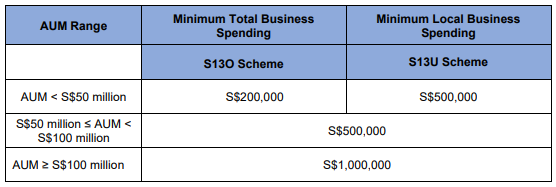

Under the updated conditions to the S13O Scheme, funds will now need to incur at least

S$200,000 in total business spending in each financial year, subject to the tiered business spending framework (set out in the table below).

Under the updated conditions to the S13U Scheme, funds will now need to incur at least S$500,000 in local business spending in each financial year, subject to the tiered business spending framework (set out in the table below).

Insofar as the terms “total business spending” and “local business spending” are concerned, the MAS has also specified that these expenditures should relate to the operating activities of the fund and do not include financing activities.

D. Local Investment

Where the S13O and S13U Schemes did not previously have any restrictions as to the geographical locations or jurisdictions to which the AUM of the funds were to be invested, the updated conditions now require that the funds will need to invest at least 10% of its AUM or S$10,000,000, whichever is lower, in local investments at any one point in time. In this regard, the MAS has specified that local investments shall include the following:

- Equities listed on Singapore-licensed exchanges;

- Qualifying debt securities;

- Funds distributed by Singapore-licensed/registered fund managers; or

- Private equity investments into non-listed Singapore-incorporated companies (e.g., start-ups) with operating business(es) in Singapore.

New Guidelines Coming into Effect

The New Guidelines will come into effect for S13O and S13U Scheme applications submitted on or after 18 April 2022. The following applications/applicants are not subject to the new conditions:

- Applications which have submitted preliminary information before 18 April 2022 and with correspondences with the MAS in the last six months; or

- Applications where the MAS had received a formal MASNET application before 18 April 2022, but which was approved after 18 April 2022; or

- Applications which were formally approved, with the issuance of a formal Letter of Offer from the MAS, before 18 April 2022.